Policy Support Indispensable For China’s Economic And Financial Recovery

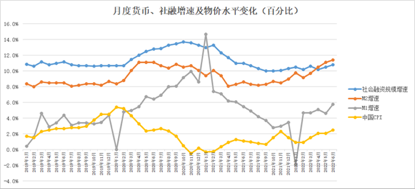

According to the latest statistics from the People’s Bank of China (PBoC), monetary and financial data showed a return to growth in June. At the end of June, the balance of broad money (M2) was RMB 258.15 trillion, a year-on-year increase of 11.4%, and the growth rate was 0.3 and 2.8 percentage points higher than that at the end of last month and the same period of the previous year respectively. Meanwhile, the balance of narrow money (M1) was RMB 67.44 trillion, a year-on-year increase of 5.8%, where the growth rate was 1.2 and 0.3 percentage points higher than the end of last month and the same period of the previous year respectively. The balance of currency (M0) in circulation was RMB 9.6 trillion, a year-on-year increase of 13.8%.

In the first half of the year, the net cash investment was RMB 518.6 billion. At the end of June, the stock of social financing was RMB 334.27 trillion, up 10.8% year-on-year, and the growth rate was 0.3 percentage points higher than that in May, though still lower than the 11% growth rate in the same period last year. The growth rates of the M2, M1 and social financing scales have all shown the tendency of increase simultaneously. Researchers at ANBOUND believe that this reflects that driven by the intensification of macroeconomic policies, the overall financial and economic situations are showing an upward recovery trend.

Figure: Monthly Monetary & Social Financing Growth Rates and Price Level Change (in percentage)

However, in terms of credit growth, which accounts for the main part of social financing and currency, the balance of RMB loans at the end of the month was RMB 206.35 trillion, a rise of 11.2% year-on-year, and the growth rate was 0.2 percentage points higher than that at the end of last month and 1.1 percentage points lower than the same period last year. In June, RMB loans rose by RMB 2.81 trillion, being a year-on-year increase of RMB 686.7 billion. This shows that despite the substantial growth of RMB credit in June and that the overall recovery has been achieved, the upward momentum remains insufficient. Continued support from macro policies will still be needed to enable China’s finance and economy to recover comprehensively. In addition, at the end of June, the balance of RMB deposits was RMB 251.05 trillion, a year-on-year increase of 10.8%, and the growth rate was 0.3 and 1.6 percentage points higher than that at the end of the previous month and the same period of the previous year respectively. In June, RMB deposits increased by RMB 4.83 trillion, a year-on-year increase of RMB 974.1 billion. The rapid growth of deposits is consistent with the previous survey results of the Chinese central bank, indicating that under the continuous impact of the COVID-19 pandemic, the market still lacks confidence in consumption and investment, which affects credit demand to a certain extent.

On the other hand, the stock of social financing at the end of June was RMB 334.27 trillion, a year-on-year increase of 10.8%. Among them, the balance of RMB loans issued to the real economy was RMB 205.09 trillion, a year-on-year increase of 11.1%. The balance of foreign currency loans issued to the real economy was RMB 2.33 trillion, a year-on-year increase of 0.5%. Entrusted loans decreased by 0.5% year-on-year, trust loans fell by 29.6% year-on-year, and undiscounted bank acceptances fell by 19.2% year-on-year. The corporate bond balance was RMB 31.48 trillion, an increase of 10.1% year-on-year. The government bond balance was RMB 57.72 trillion, up 19% year-on-year. The domestic stock balance of non-financial enterprises was RMB 9.96 trillion, a year-on-year increase of 14%.

The cumulative increment of social financing in the first half of 2022 was RMB 21 trillion, which was RMB 3.2 trillion more than the same period last year. Among them, RMB loans issued to the real economy increased by RMB 13.58 trillion, a year-on-year increase of RMB 632.9 billion. Foreign currency loans issued to the real economy increased by RMB 45.8 billion, a year-on-year decrease of RMB 182.3 billion. The entrusted loans decreased by RMB 5.4 billion, which was a year-on-year decrease of RMB 109.1 billion; while trust loans decreased by RMB 375.2 billion, making it a year-on-year decrease of RMB 348.7 billion. Undiscounted bank acceptance bills decreased by RMB 176.8 billion, a year-on-year decrease of RMB 171.4 billion. Corporate bond net financing was RMB 1.95 trillion, a year-on-year increase of RMB 391.3 billion. The net financing of government bonds was RMB 4.65 trillion, an increase of RMB 2.2 trillion year-on-year. Additionally, the stock financing of non-financial enterprises in the country was RMB 502.8 billion, an increase of RMB 7.3 billion year-on-year.

These data changes reflect that the scale of social financing in May and June has increased significantly under the circumstance that monetary policy easing has intensified since the second quarter. The increase in the scale of social financing in June reached RMB 5.17 trillion, an increase of RMB 1.47 trillion year-on-year. The stock of social financing has basically filled the gap left by the sharp decline in social financing in March and April, and the overall social financing has seen a recovery to the long-term trend. In realizing the incremental recovery of the social financing scale, it should be pointed out that government bond financing has played a major role, and its incremental growth has reached RMB 2.2 trillion. In fact, this was essentially driven by the massive issuance of local government bonds in May and June. It has been estimated that in June alone, the incremental scale of government bond financing reached RMB 1.6 trillion, which is a significant continuous increase from RMB 1 trillion in May. This has played a major role in the RMB 3.3 trillion increase in the scale of social financing. Furthermore, the decline in non-standard financings such as entrusted loans, trust loans, and bank drafts is due to the substitution effect brought about by credit easing on the one hand, and this is closely related to the effect of the shrinking real estate market on the other hand. In the first half of the year as a whole, the rise of RMB 13.58 trillion in credit to the real economy, which was an increase of RMB 632.9 billion year-on-year, also means that the central bank’s sustained goal of maintaining credit growth has been achieved.

For the growth rate of the social financing scale to be 10.8%, this would signify that China’s timely adjustment of monetary policy in the first half of the year has a positive effect on stabilizing the country’s finance and on promoting stable growth. This may be the basis for the PBoC to emphasize the return to stabilization policy. As far as the second half of the year is concerned, the scale of social financing is still under great pressure to maintain the growth rate. This is especially true when the peak of local bond issuance has passed and the quota has been exhausted. The issuance of government bonds, which played a supporting and bottom-up role for social growth in the first half of the year, will then see a decline in its effect. This, in turn, will increase the reliance on RMB loans or other direct financings for social financing growth. Promoting the growth of bank loans will remain the main task in the future. In other words, China’s macroeconomic policies such as monetary and fiscal policies still need to provide continuous support for economic recovery through total easing and structural adjustment.

Final analysis conclusion:

In June, the growth rate of monetary and social financing in China showed a simultaneous increase, indicating that the overall financial and economic situations of the country are showing a recovery trend. This, all in all, is driven by the intensification of macroeconomic policies. Nonetheless, under the circumstance of the withdrawal of local government bond issuance, there will still be pressure to maintain the continued growth momentum of monetary and social financing in the future. Hence, the ongoing support from macro policies will become indispensable.