Where China Gets Its Oil: Crude Imports in 2025 Reveal Stockpiling and Changing Fortunes of Certain Suppliers, Including Those Sanctioned

- China’s crude oil imports hit a record-high 11.6 million barrels per day in 2025, as geopolitical tensions, low oil prices, and global oversupply spurred China to increase its oil stockpiles, a trend likely to continue in 2026.

- The large volume of oil China has in storage means it would likely be able to weather any multi-month disruption of its imports from Iran and Venezuela, which supplied about 15 percent of China’s crude imports last year.

- Indonesia and Brazil accounted for almost all the increase in China’s oil imports in 2025; Brazil’s production growth and status as a low-risk supplier contributed to a 28 percent increase in its deliveries to China, while the rebranding of some Iranian crude as Indonesian probably explains the 98-fold increase in Indonesia’s exports to China.

The Trump administration’s imposition of sanctions on Russian oil companies Rosneft and Lukoil in October, intervention in Venezuela in January, and threats to take military action against Iran have focused attention on China, the top crude customer of all three countries. China relied on sanctioned crudes from Iran, Russia, and Venezuela for a significant share of its crude imports in 2025. How much crude China buys from these countries has implications for other oil exporters that supply China.

In this Q&A, Senior Research Scholar Dr. Erica Downs analyzes China’s crude oil imports in 2025, including sanctioned supplies, and how the country would manage a disruption of its Iranian and Venezuelan crude flows. She finds that sanctioned crudes (including Russian barrels) probably accounted for more than one-fifth of China’s imports and affected other suppliers, contributing to increased imports from Brazil and Indonesia and decreased purchases from Oman. China’s oil stockpiles should enable it to weather any multi-month interruption of its imports.

Why did China import a record-high amount of crude oil in 2025?

Stock building. China’s crude imports grew from 11.1 barrels per day (bpd) in 2024 to 11.6 in 2025. According to Rystad Energy, China stockpiled 430,000 bpd last year, 83 percent of the increase in China’s crude imports. Geopolitical risks, global oversupply, and low oil prices spurred China to increase its stockpiles. China’s heavy reliance on imported oil (over 70 percent of consumption), especially seaborne imports (over 90 percent of total imports), has made oil stockpiling a cornerstone of China’s approach to oil security.

China’s stock building is likely to continue in 2026. China’s national oil companies (NOCs) plan to build at least 169 million barrels of new storage capacity in 2025–2026. Filling this capacity would help absorb the “deep surplus” of global oil supplies in the first quarter of 2026.

Which countries were China’s largest crude oil suppliers?

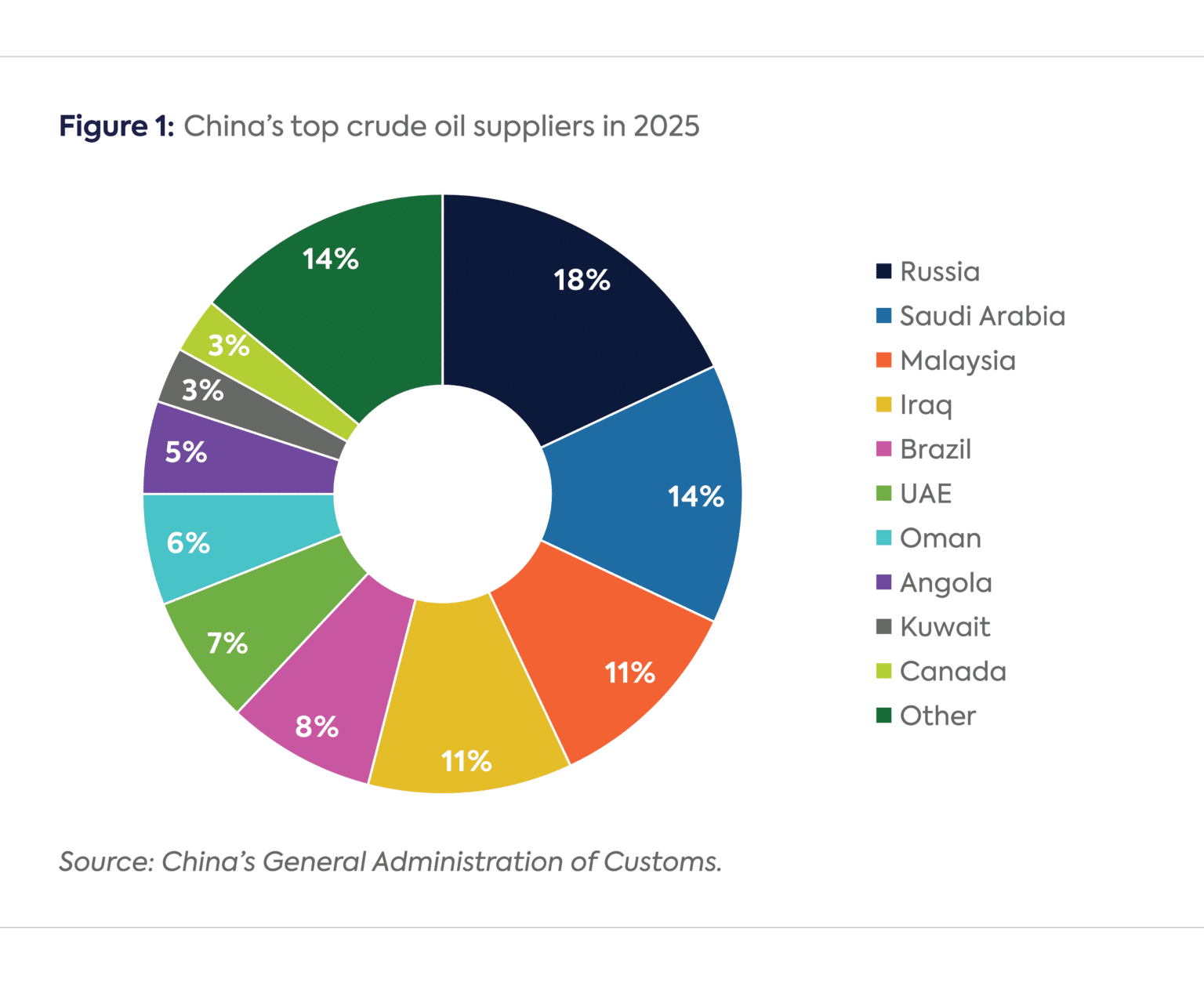

According to China’s General Administration of Customs (GAC), five countries—Russia, Saudi Arabia, Malaysia (likely sanctioned barrels), Iraq, and Brazil—accounted for 62 percent of China’s crude imports in 2025 (see Figure 1). Two countries “missing” from China’s top ten suppliers are Iran and Venezuela. GAC has not recorded any oil imports from Iran since 2022 and reported imports of less than 7,000 bpd from Venezuela last year. However, tanker tracking shows the volumes from these countries are much higher.

How much sanctioned oil did China import from Iran, Venezuela, and Russia last year?

China probably imported at least 2.6 million bpd of sanctioned crudes in 2025, over 22 percent of total imports. This estimate includes 1.38 million bpd from Iran and 389,000 bpd from Venezuela, according to Kpler, and at least 800,000 bpd of oil from Russia. It is difficult to determine exactly how much crude the Russian oil companies sanctioned by the United States—Rosneft, Lukoil, Surgutneftegaz, and Gazprom Neft—shipped to China because there is no publicly available, official data that show Russian exports to China by company.[1] However, Rosneft exports 200,000 bpd to China via the Kazakhstan-China oil pipeline and probably most of the 600,000–700,000 bpd sent to China via the ESPO pipeline spur.

The gap between Kpler’s data on China’s Iranian and Venezuelan crude imports and that of China’s GAC is because Iranian and Venezuelan barrels are relabeled to disguise their origins. Many Iranian and Venezuelan barrels that arrive in China are rebranded as Malaysian. China imports more “Malaysian” crude (1.3 million bpd in 2025) than Malaysia produces (535,000 bpd in 2024), and the waters off Malaysia are a hotbed of ship-to-ship (STS) oil transfers.

Were there notable changes to China’s oil import portfolio in 2025?

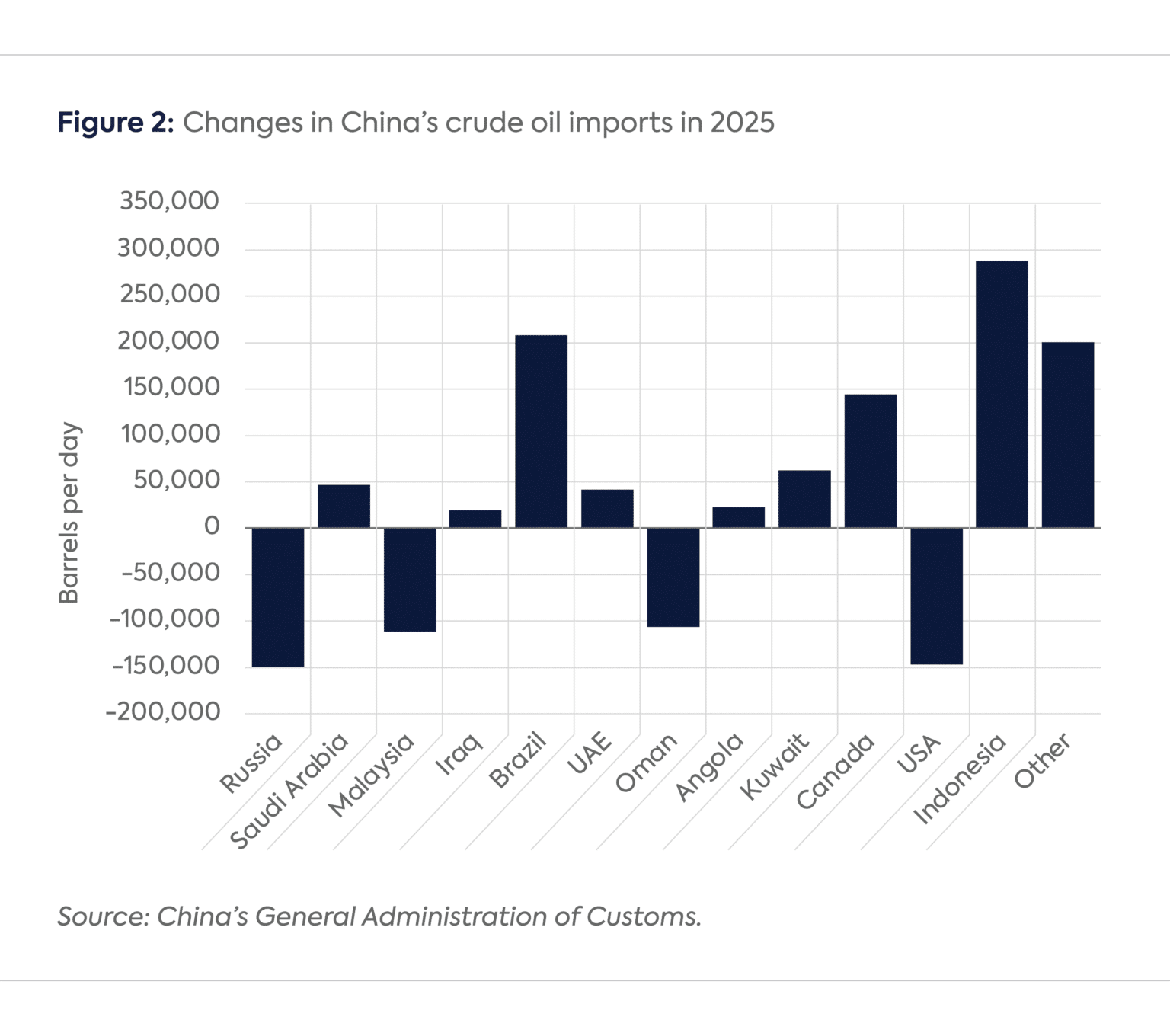

Although Russia and Malaysia maintained their positions as China’s largest and third-largest suppliers, respectively, both countries sent less oil to China in 2025 than in 2024 (See Figure 2).

Russia’s crude exports to China fell by 150,000 bpd (6.9 percent). New sanctions prompted China’s NOCs to reduce their imports from Russia, while China’s teapot refineries, the main buyers of Russian seaborne crude, opted to purchase more Iranian barrels because of the more attractive pricing.

Malaysia’s oil exports to China fell by 112,000 bpd (7.9 percent). Malaysia announced in July 2025 that it would fully enforce new rules aimed at preventing illegal STS oil transfers, which perhaps prompted traders to relabel sanctioned crudes as originating from other countries.

Indonesia and Brazil accounted for over 95 percent of the growth in China’s crude imports. As noted, the surge in Indonesia’s exports to China from less than 3,000 bpd to 291,000 bpd probably is because some Iranian crude was rebranded as Indonesian. Indonesia is a net oil importer, and it exported 73,000 bpd in 2024. Brazil’s increasing production and China’s view of the country as a reliable supplier likely contributed to the 28 percent (208,000 bpd) increase in Brazil’s exports to China.

Canada and the United States experienced diverging fortunes. Trade tensions contributed to the 76 percent (147,000 bpd) plunge in China’s imports of US crude. The increase in Canada’s exports to China (144,000 bpd) offset the decline in US deliveries. Chinese imports of Canadian heavy crude are likely to keep growing as a feedstock for increasing petrochemical output.

China’s imports from Oman fell by over 100,000 bpd. This may reflect discounts on sanctioned Iranian barrels. Reuters calculated that Iranian Light crude is $8 to $10 per barrel cheaper than Omani crude.

How would China respond to a major disruption of its Venezuelan and Iranian oil imports?

China’s oil stockpiles and crude in storage in Asia and on the water leave it well positioned to weather a multi-month disruption. As of early January, China had 1.206 billion barrels of oil in storage onshore, which would cover 104 days of net crude oil imports at the 2025 level.

There also are likely ample supplies of Venezuelan and Iranian crudes on the water. In early January, more than 29 million barrels of Venezuelan crude and 170 million barrels of Iranian crude and condensate were on tankers or floating storage. There are also Iranian barrels in bonded storage in Chinese ports.

The Chinese refiners likely to be the most adversely affected by a prolonged disruption of Iranian and Venezuelan crude exports are the teapots. They are the main buyers of Iranian and Venezuelan oil because they are more risk tolerant than China’s NOCs and depend on the discounts to bolster their bottom lines. If the teapots were unable to access Iranian and Venezuelan crudes, they would likely purchase more Russian oil and perhaps more Canadian heavy crude, which Argus says is the most cost competitive unsanctioned crude for China.